tax advice please on lump sum

happyfella

Online Community Member Posts: 519 Empowering

hi, we are trying to work out our finances. My wife who will be 65 in august will be receiving a lump sum pension of £6,000 in august. She works and comes out with £770 every four weeks. i do not work as i receive full pip for both and unable to work. i have just checked on the tax calculator and it says when my wife receives her lump sum she will have to pay £1,400 tax on it. can i confirm that is correct, and also can i ask, if they will take it in one go from her pension pot or will they take it each month from her wage. at the moment she does not pay tax due to how little she earns. will this lump sum also affect her receiving the carers element on universal credit. any advice would be great, as we are trying to plan for the future.

0

Comments

-

hi, sorry, yes that is the full value of the pension pot. her normal yearly wage is £10,100 her pension is with her currently employer through legal and general

0 -

I took my pension pot out last year it was 12,000 but I received 10,000 mine was tesco pension0

-

lisathomas50 said:I took my pension pot out last year it was 12,000 but I received 10,000 mine was tesco pension

what age are you if you dont mind me asking, and did you carry on working at tesco. my wife works there, and this is the second pension. she receives £90 a month from the first pension pot, so she wants to take it all for the second pension, but does not want to be hit with a big tax bill.

0 -

Remember that if the lump sum together with any existing savings takes your joint savings over £6000 you need to inform UC.

The inclusion of the carer element in your UC calculation is not affected0 -

calcotti said:Remember that if the lump sum together with any existing savings takes your joint savings over £6000 you need to inform UC.

The inclusion of the carer element in your UC calculation is not affected

thank you.

0 -

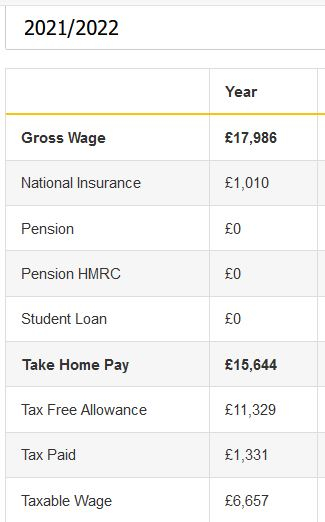

it is before tax. it is a private and work pension. what i did ref the tax, i put it in a tax website. i added her wages for the year and then added the lump sum on top and it come out with £1,400 tax

0 -

what i did was to add the pension together and my wifes wages and then the lump sum using this https://www.moneysavingexpert.com/tax-calculator/ and this is what it came out with, but i will speak to legal and general. so i added her 4 weekly wage, to her pension, and then the lump sum.

0 -

I left tesco didn't work for 6 months then I did another job I took it out when I was 55 I now have another pension0

-

Happyfella, if the £6000 is the gross amount of the pension payment and 25% will be tax free then you should only take £4600 into account when calculating the tax liability.

Also, you should put that figure in the pension box, not the wage box (because NI is calculated on the wage but is not due on the pension).

Don’t know where tax free allowance of £11,329 comes from. Tax free allowance for 2021-22 is £12,570. Does she have other circumstances that reduce her allowance?0 -

calcotti said:Happyfella, if the £6000 is the gross amount of the pension payment and 25% will be tax free then you should only take £4600 into account when calculating the tax liability.

Also, you should put that figure in the pension box, not the wage box (because NI is calculated on the wage but is not due on the pension).

Don’t know where tax free allowance of £11,329 comes from. Tax free allowance for 2021-22 is £12,570. Does she have other circumstances that reduce her allowance?

thank you for that.

0

Categories

- All Categories

- 15.8K Start here and say hello!

- 7.6K Coffee lounge

- 106 Games den

- 1.8K People power

- 160 Announcements and information

- 25.3K Talk about life

- 6.2K Everyday life

- 508 Current affairs

- 2.5K Families and carers

- 873 Education and skills

- 2K Work

- 580 Money and bills

- 3.7K Housing and independent living

- 1.2K Transport and travel

- 643 Relationships

- 1.6K Mental health and wellbeing

- 2.5K Talk about your impairment

- 879 Rare, invisible, & undiagnosed conditions

- 941 Neurological impairments and pain

- 2.2K Cerebral Palsy Network

- 1.3K Autism and neurodiversity

- 40.8K Talk about your benefits

- 6.1K Employment & Support Allowance (ESA)

- 20.3K PIP, DLA, ADP & AA

- 9.1K Universal Credit (UC)

- 5.3K Benefits and income